Deal activity in the technology industry has seen a surge in SaaS acquisitions (55% of all software deals in 2023). Additionally, 67% of TMT leaders plan to improve technology processes using M&A, which is expected to be SaaS deals. So, what are the main trends in SaaS M&A, and where is it all going? This article delves into the following topics:

- Top 10 SaaS M&A players

- Top 10 SaaS M&A deals of 2023

- Top insights for SaaS corporate acquirers

SaaS M&A transactions overview: Key players

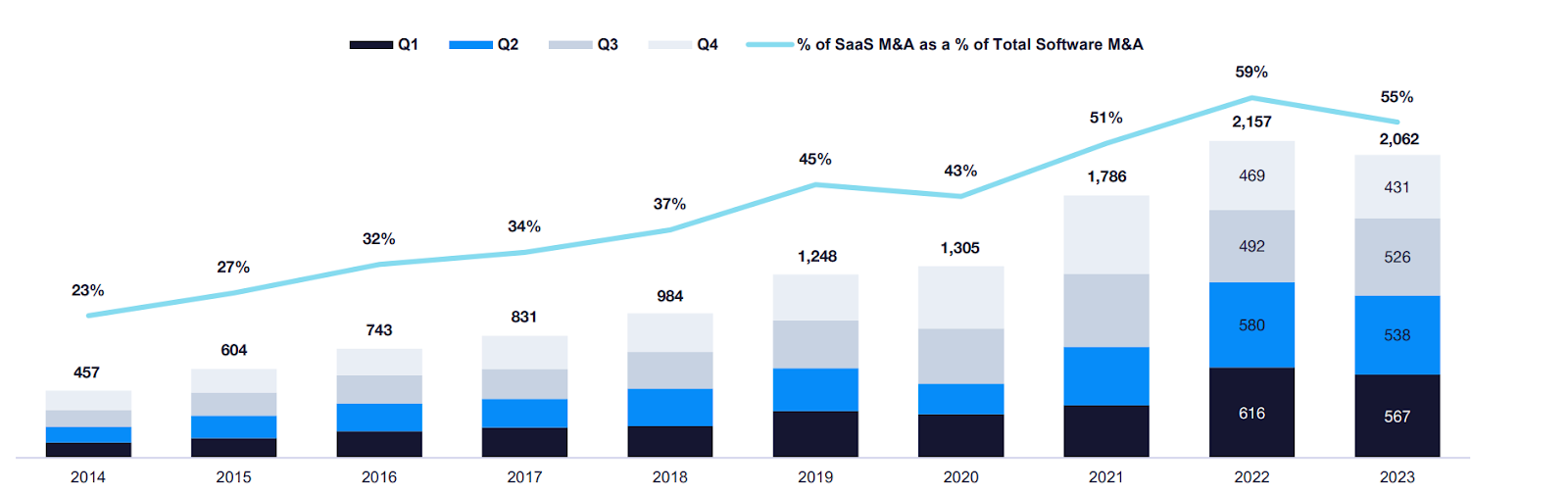

SaaS M&A activity showed resilience in 2023, totaling 2,062 deals. It was the second most active year since 2014.

Source: Software Equity Group (SEG)

Both strategic buyers and private equity firms pursued well-selected acquisitions to strengthen tech capabilities in small business verticals. Key SaaS M&A players were the following.

| Strategic buyer | 2023 deal volume | Notable acquisition |

| Constellation Software | 25 | WideOrbit: $1.6 billion |

| Valsoft Corporation | 24 | FuturaSi: Undisclosed |

| Visma | 15 | Xubio: Undisclosed |

| Cisco | 11 | Splunk: $28 billion |

| Aptean | 7 | 3T Logistics: Undisclosed |

| Private equity firm | 2023 deal volume | Notable acquisition |

| Main Capital Partners | 10 | WeFact: Undisclosed |

| Francisco Partners | 7 | New Relic: $6.5 billion |

| Thoma Bravo | 6 | Nextgen Healthcare: $1.8 billion |

| Vista Equity Partners | 5 | EngageSmart: $4 billion |

| TPG Capital | 4 | Nextech: $1.5 billion |

Top 10 SaaS M&A deals

You can see the ten notable take-private and public SaaS acquisitions by the most active strategic and private equity buyers of 2023. Let’s start with strategic buyers first.

Strategic buyers

Some notable SaaS acquisitions by strategic buyers were the following:

- Cisco + Splunk

- Constellation Software + WideOrbit

- Visma + Xubio

- Valsoft Corporation + Futura

- Aptean + Prima Solutions

Cisco + Splunk

| Cisco info |

| Cisco Systems is one of the biggest publicly traded SaaS companies with $197 billion in market cap and $57+ billion in revenue. It offers networking equipment, cloud computing, and cybersecurity SaaS solutions. |

| Splunk info |

| Splunk is a U.S.-based cybersecurity software company with over $26 billion in market cap and over $3.9 billion in revenue. |

| M&A value |

| Cisco Systems announced the 28-billion, all-cash acquisition of Splunk in September 2023. One of the largest public SaaS company acquisitions is expected to close at the end of Q2 2024. |

| M&A rationale |

| Portfolio extension. Splunk’s cloud apps, API services, data centers, and security applications strengthen Cisco’s product portfolio. Cloud revenue growth. The acquisition will generate ~ $4 billion in recurring subscription revenue for Cisco. Strong market position. Cisco aims to strengthen its strategic position while anticipating revenue growth due to increasing cybersecurity spending. |

Constellation Software + WideOrbit

| Constellation Software info |

| Constellation Software is a Canadian holding company with over $79 billion in market cap and over $7 billion in revenue. It acquires and develops vertical software companies. |

| WideOrbit info |

| WideOrbit is a U.S. advertisement management software company with over $140 million in revenue. It provides business intelligence, ad management, and billing automation solutions. |

| M&A value |

| Constellation Software acquired WideOrbit for $1.6 billion in cash and company stock in February 2023. |

| M&A rationale |

| Market exposure. WideOrbit is a global sell-side advertising processor with 20 years of experience and over 6,000 customers, including TV, radio, and cable network providers. Revenue growth. WideOrbit systems have processed over $38 billion in advertisement spending. It’s a promising target for Constellation Software. |

Visma + Xubio

| Visma info |

| Visma is a Norwegian technology company with over €2 billion in revenue and over 1.7 million customers. It offers accounting, HRM, and payroll software for the corporate and public sectors. |

| Xubio info |

| Xubio is an Argentina-based provider of ERP cloud software with over $16 million in revenue (ZoomInfo). |

| M&A value |

| Visma acquired Xubio for an undisclosed amount in January 2023. |

| M&A rationale |

| Market share expansion. Xubio serves over 50,000 SMEs in Latin America, which is a considerable addition to Visma’s target audience in said region. Product expansion. Visma has access to Xubio’s impressive financial technology stack, ranging from billing tools to financial reporting solutions. |

Valsoft Corporation + Futura

| Valsoft Corporation info |

| Valsoft Corporation is a Canadian holding company. It has established strategic alliances with over 90 software companies in 25+ industries across 14+ countries. |

| FuturaSi info |

| FuturaSi is an Italian provider of cloud software for heating systems with over $6 million in revenue (ZoomInfo). It offers maintenance planning, data analytics, and warehouse management solutions. |

| M&A value |

| Valsoft Corporation acquired FuturaSi for an undisclosed amount in January 2023. |

| M&A rationale |

| Market expansion. FuturaSi provides exposure to the European service and maintenance market. Product expansion. FuturaSi offers seven warehouse maintenance tools, providing Valsoft a solid basis for making it a powerful, more complete solution. |

Aptean + Prima Solutions

| Aptean info |

| Aptean is a leading provider of enterprise software in the U.S. with over $600 million in revenue (ZoomInfo). |

| 3T Logistics info |

| 3T Logistics is a British transportation software company with $18 million in revenue (ZoomInfo) that delivers logistics management and automation solutions. |

| M&A value |

| Aptean announced the acquisition of 3T Logistics for an undisclosed amount in November 2023. |

| M&A rationale |

| New capabilities. Aptean extends its transportation management systems (TMS) products and leverages 3T Logistics’s AI capabilities for generating long-term revenue in the European market. Market exposure. 3T Logistics gives Aptean more exposure to industrial machinery, automotive, consumer goods, construction, and food & beverage sectors. |

Private equity firms

Notable acquisitions by institutional buyers include the following:

- Francisco Partners + New Relic

- Vista Equity Partners + EngageSmart

- Thoma Bravo + Nextgen Healthcare

- TPG Capital + Nextech Systems

- Main Capital Partners + WeFact

Francisco Partners + New Relic

| Francisco Partners info |

| Francisco Partners is a U.S.-based technology-focused private equity firm that has raised over $45 billion in 400+ transactions. |

| New Relic info |

| New Relic is a U.S.-based digital intelligence provider with over $900 million in revenue. It uses over 30 digital capabilities, including AI monitoring, and over 700 integrations. |

| M&A value |

| Francisco Partners completed an all-cash, take-private acquisition of New Relic for $6.5 billion in November 2023. |

| M&A rationale |

| Business growth. Francisco Partners emphasizes innovation opportunities while funding and developing SaaS companies. Investor returns. Francisco Partners has generated over $35 billion in revenue across its portfolio companies. |

Vista Equity Partners + EngageSmart

| Vista Equity Partners info |

| Vista Equity Partners is a U.S.-based private equity firm with over $100 billion in assets under management. It has invested in over 85 software companies across 25 industries. |

| EngageSmart info |

| EngageSmart is a U.S.-based software company with over $300 million in revenue that provides client engagement and payment automation solutions. |

| M&A value |

| Vista Equity Partners acquired EngageSmart for ~ $4 billion in January 2024, in a take-private deal. EngageSmart was delisted from public markets. |

| M&A rationale |

| Market growth. Vista Equity Partners leveraged investment experience to develop EngageSmart further and grow its market presence. |

Thoma Bravo + Nextgen Healthcare

| Thoma Bravo info |

| Thoma Bravo is a U.S.-based private equity firm with over $130 billion in assets under management and control investments in 75 portfolio companies. |

| Nextgen Healthcare info |

| Nextgen Healthcare is a U.S.-based EHR software company with over $700 million in revenue. |

| M&A value |

| Thoma Bravo acquired Nextgen Health for $1.8 billion in an all-cash take-private deal in November 2023. |

| M&A rationale |

| Long-term growth. Thoma Bravo helps Nextgen develop new products using its rich investment management expertise. High market exposure. Nextgen serves over 10,000 ambulatories and 65 million patients across the United States. Revenue growth. Thoma Bravo anticipates increasing SaaS revenues amid an active transition to value-based care (VBC), which is projected to grow by 50% in the upcoming years. |

TPG Capital + Nextech Systems

| TPG Capital info |

| TPG Capital is a U.S.-based private equity firm with over $222 billion in assets under management and over 300 active portfolio companies. |

| Nextech Systems info |

| Nextech Systems is a U.S.-based EHR software company with over $100 million in revenue focused on cosmetic surgery, noninvasive treatments, and SPA. |

| M&A value |

| TPG Capital acquired Nextech Systems for around $1.5 billion in June 2023. |

| M&A rationale |

| Market exposure. Nextech serves over 11,000 healthcare professionals in 66,000 clinics, providing TPG exposure to dermatology, SPA, plastic surgery, ophthalmology, and orthopedics niches. Portfolio expansion. TPG aims to capitalize on telehealth and data analytics opportunities in prospective healthcare niches. |

Main Capital Partners + Wefact

| Main Capital Partners info |

| Main Capital Partners is a Dutch private equity firm with over €2.1 billion in assets under management and over 71 portfolio companies. |

| WeFact info |

| WeFact is a Dutch SME cloud software provider that delivers invoicing and accounting solutions. |

| M&A value |

| Main Capital Partners acquired the majority stake (undisclosed amount) in WeFact in January 2023. |

| M&A rationale |

| Business development. Main Capital Partners actively invests in small and middle-market software companies in the $3 – $100 million revenue range and strong growth opportunities. Market share growth. WeFact serves over 10,000 businesses in Europe, offering Main Capital Partners new opportunities in the European market. |

Top SaaS M&A insights

Here are several SaaS M&A industry highlights:

- The global SaaS M&A volumes have increased 4.5 times in absolute values in the past ten years, averaging 16.6% YoY growth. At the same time, SaaS IPO’s volume has declined since 2021.

- The global SaaS sector constituted 16% of all technology and media deals and 3.7 % of all M&A deals in 2023.

- Sales & marketing, data analytics, and content & workflow management product categories accounted for 39% of the total SaaS M&A volume in 2023.

- As much as 48% of buyers acquired vertical targets, with healthcare and financial deals being the most popular.

- 2023 SaaS buyers prioritized smaller acquisitions (with a few exceptions) as the 2023 median acquisition price dropped over 27% YoY across TMT deals.

- Buyers also valued targets more conservatively in 2023 as the median SaaS revenue multiples decreased by 27% YoY.

The bottom line

- Most SaaS M&A buyers switched from mega deals to smaller, narrow-niche acquisitions in uncertain market conditions.

- Sales & marketing tech, data analytics, AI capabilities, and workflow management tools in healthcare and financial sectors dominated the 2023 SaaS M&A landscape.

- Most 2023 M&A buyers aimed at strengthening tech capabilities and market presence in specific business verticals.